Fx Swap

FinPricing offers:

Four user interfaces:

- Data API.

- Excel Add-ins.

- Model Analytic API.

- GUI APP.

FinPricing provides valuation tools for the following FX products:

| 1. Currency Swap Introduction |

An FX swap or currency swap is a contract in which both parties agree to exchange one currency for another currency at a spot FX rate. The agreement also stipulates to re-exchange the same amounts at a certain future date also at a FX forward rate.

Many people confuse currency swaps with cross currency

swaps. They are totally different. A cross currency swap is an interest rate swap in which

two parties to exchange interest payments and principal on loans denominated in two different currencies.

In a currency swap, one party simultaneously borrows one currency and lends another currency to a second party. The repayment obligation is used as collateral and the amount of repayment is fixed at the FX forward rate.

FX swaps can be considered riskless collateralized borrowing/lending.

The contract virtually allows you to utilize the funds you have in one currency to fund obligations denominated in

a different currency, without incurring foreign exchange risk.

A currency swap is a simultaneous purchase and sale of identical amounts of one currency for another with two

different value dates, normally spot to forward. Therefore, an FX swap consists of two transactions: a spot transaction

and a forward transaction. Effectively the FX swap is two exchange contracts packed in one: a spot foreign exchange

transaction and a forward FX transaction.

A currency swap deal can be used if you have a currency, which you do not need before a certain time, but at the

same time have a short-term need for another currency. Swap deals are used for managing currency risks, postponing

the term of forward-deal and optimizing financing.

The most common use of FX Swaps is for institutions to fund their foreign exchange balances. FX swaps are also used

by importers and exporters, as well as institutional investors who wish to hedge their positions. They are also used

to speculate and, by incurring a risk, attempt to profit from rising or falling exchange rates.

Currency swaps are OTC trades and have credit risk. In the case that one of the parties is

unable to fulfill its obligation, the other party will have to sign another contract with a third party, thus being

exposed to market risk at that time.

| 2. Forex Market Convention |

One of the biggest sources of confusion for those new to the FX market is the market convention. We need to make clear the meaning of the following terms in the forex market first.

| 3. Pricing FX Swap |

An FX swap is a simultaneous purchase and sale of identical amounts of one currency for another with two different

value dates, normally spot date and forward date. Therefore, an FX swap has two legs – a spot transaction and a forward

transaction.

In the spot leg, a particular quantity of a currency is bought or sold versus another currency at an agreed upon rate on the spot date.

In the forward leg, the same quantity of currency is then simultaneously sold or bought versus

the other currency at a second agreed upon rate on the forward date.

From valuation perspective, an FX swap can be viewed as a combination of two

FX forward contracts. In general, it has a long

FX forward contract and a short one.

Typically, one leg of the outstanding contract would

have already expired. Therefore, in many situations, an FX swap is equivalent to an

FX forward contract.

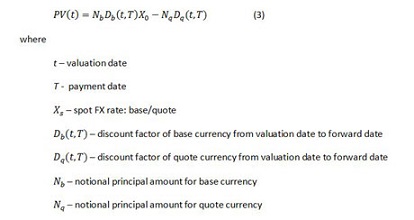

The present value of a currency forward contract is given by

| 5. Related Topics |