Barrier Option

FinPricing offers:

Four user interfaces:

- Data API.

- Excel Add-ins.

- Model Analytic API.

- GUI APP.

FinPricing covers the following barrier option models:

A barrier option, or a single barrier option, is a financial contract that gives the holder the right to buy or sell an underlying asset when the price of the underlying asset reaches a certain level.

There are two fundamental types of barrier options: knock-in barrier options and knock-out barrier options.

Knock-In barrier option needs to come into existence first before expiration. A knock-in barrier option is activated or knocked-in when the underlying asset price hits the barrier. If the option has never crossed the barrier, the option is eliminated and the holder will receive a rebate.

Knock-Out barrier option is similar to a regular vanilla option except that it becomes worthless if the underlying asset price touches the barrier. In other words, if a knock-out option's underlying touches the barrier, the option is eliminated and the holder receives a rebate.

Barrier options have become very popular path-dependent options since first traded in both exchanges worldwide and in over-the-counter (OTC) markets. Because they are not only cheaper than regular vanilla options, but also very flexible in setting the barrier levels. Furthermore, they are able to be linked to any underlying securities. Many structured financial products have barrier provisions.

Barrier options are very useful tools for hedging risk. For instance, A down and in put option provides a cheap protection for downside movement, while an up and out call may offer an expensive enhancement for existing long position.

There are eight different types of single barrier options:

A "out" option becomes a simple European style option, provided that the value of the underlying asset remains above the barrier level over the entire option tenor. When the barrier is crossed, the option ceases to exist i.e., “knocks out”); moreover, a rebate is paid to the option holder immediately upon knockout. If the payoff is the same as that for a vanilla call and the barrier level is lower, the barrier option is termed a down and out call. Similarly, we can define up and out call, down and out put and up and out put options.

A "in" option exires worthless unless the underlying asset price hits the barrier before expiry. If the asset value reaches the barrier level at some time prior to expirty then the option becomes a vanilla option with a payoff. If the payoff is the same as a vanilla call and the level is a low barrier, it is a down and in call. If the payoff is that of vanilla call and the level is a high barrier, it is an up and in call. Down and in put and up and in put can be defined in an analogous way.

Most barrier options are discrete options as the barrier even is normally monitored at discrete time. However, in current market, the barrier is commonly monitored near continously.

If the option hits the barrier while being in the money, we call it reverse barrier option. Otherwise, it is a regular barrier option. In other words, regular knock-in and knock-out barrier options are out-of-money but reverse knock-in and reverse knock-out options are option in the money.

The behaviour of reverse knock-in/reverse knock-out is very different from regular knock-in and knock-out. The owner of a reverse knock-out, for example, shows a large intrinsic option value just before the time the barrier is hit. Also, as expiry approaches, reverse barriers start behaving as pure digitals!

If the touch condition is satified, the profile could be either flat if the payout is cash or a straight line with slop 1 if the payout is asset.

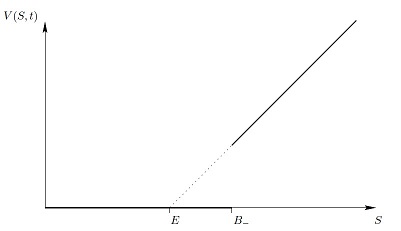

The payoff of a Down and Out call option is equal to the vanilla call payoff at expiry if it survives and vanishes on the barrier. The payoff diagram is shown below where B is the barrier and E is the strike.

A Down and In call option specification, for example, includes the exercise type (i.e., either American or European), an exercise time T, a strike level K, a rebate value R and a barrier level H, which depends continuously on time over the interval [0, T].

Here the underlying security is any security whose price S can be modeled as a piecewise geometric Brownian motion over the life of the option. In addition we require that the initial spot level for the underlying security S(0) lie above the initial barrier level H(0).

The payoff for a Down and In call is that of a standard European call, provided that the underlying falls below the barrier level at some time during the option’s life; otherwise, the payoff at expiry is equal to the fixed rebate R. Formally a long European Down and In call option payoff is defined at exercise time T as

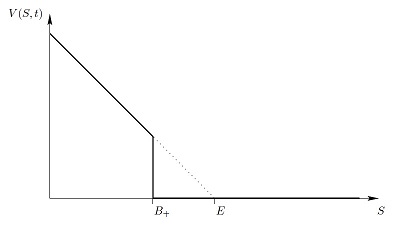

A Down and Out put option is knocked out worthless if the underlying asset falls to the barrier. However, if it does not, the holder receives the payoff of a vanilla put option. Obviously the vanilla put must be struck above the barrier. If it is struck below the barrier, the option does not pay out either at expiry or at the barrier. The payoff diagram of a Down and Out put option is displayed below:

Up and Out/In options' analytics are similar to their down dounterparts. For example, a Up and Out put option is very similar to a Down and Out call. If the barrier is set above the strike, it reflects the vanilla put option in the barrier. If the barrier is below the strike, the payoff is truncated. The payoff diagram of a Up and Out put is shown below.

Interest rates apply from spot date to delivery date. The interest rate curve is a curve relative to spot date, not valuation date. In other words is a forward curve from valuation date point of view. This is in clear contrast to valuation date perspective needed in accounting

Barrier options are path-dependent. Analytic formulas for pricing barrier options do not exist for the case where the barrier is an arbitrary, or discrete, or of discrete dividends. Tree methods (e.g., trinomial or binomial) can, however, be used to approximate the price of barrier options.

Unfortunately standard tree methods, when applied to price barrier options, suffer from several drawbacks, that is, these methods may converge very slowly and/or display a persistent bias in the price. Therefore, PDE is probably the best solution for all kinds of single-asset barrier options.

In contrast a long American Down and In call can be exercised immediately after it has knocked); if the option does not knock in, then the fixed rebate R is received at maturity.

Assume that the underlying price follows a log-normal distribution. Based on the assumption, we evaluate the European style payoffs for the single barrier option types above using analytical formulae. We note, since barrier option payoffs are path dependent, that a more accurate option pricing treatment should incorporate respective time varying short-interest rate and volatility.

In some special cases,there is analytial solution for vanilla single barrier option that assumes that barrier is continuously monitored.

When the price nears the barrier and the option is about to expire, the Delta and Gamma of an up-and-out call takes large negative values because the option payoff turns into a spike in this region. Vega also turns negative when the price of the underlying asset is close to the barrier because a volatility pickup near the barrier increases the likelihood of the price passing through it.

Barrier option usually has a very large gamma that makes hedge very difficult. If the underlying is near the barrier when expiry approaches, the option value can have two quite different possible outcomes. The price jump causes discontinuition. In this case, a barrier shifting technique is required to manage the discontinuity risk.

Another type of barrier option is called partial barrier option. These options are similar to ordinary barrier options except that the barrier extends either from the beginning of the life of option until a window end, or from the window end until the maturity of the option. This type of options cares only whether in the window the asset price is above or below the barrier at any time, not whether the barrier is actually crossed.

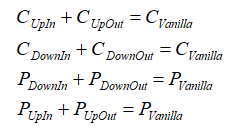

Option put-call parity represents the relationship between European call option and put option. The symetry is very useful in valuation and hedging. Similarly, there are in-out parity symetry among barrier options. The in-out parity among knock-in, knock-out, and vanilla options is given by

Put-Call parity tells us that no matter what pricing algorithm is employed, those relation must hold at price level, otherwise there will be an arbitrage opportunity. Moreover, this parity relationship should hold for Greeks too.

In FX market, if you are using a close-form solution, also called modified Black Scholes, to price a first generation exotic option (e.g., barrier option), you may need to apply Vanna-Volga adjustment to the Black Scholes theoretical price because the close-form approach is inaccurate for exotic products.

The idea is that the total hedge cost between the cost of the hedge on spot rate and the cost of hedge on volatility can be separated. The first part is the price of the same barrier option using the Black Scholes hypothesis. The second part is computed as the difference between hedging the volatility sensitivities (Vega, Vanna and Volga) using strategies composed out of smiled options and the same strategies priced with the ATM volatility. The most liquid FX market quotes are ATM volatility, 25% delta Risk Reversal and 25% delta Butterfly.

To do the adjustment, one first needs to compute the price and the volatility sensitivities of this barrier option using ATM volatility, and then compute the price and volatility sensitivities of the three different instruments (ATM call/put option, 25% delta Risk Reversal, 25% delta Butterfly) using ATM volatility.

The surplus of cost generated by the hedging portfolio is then computed as

If you are using an advanced numerical solution that captures the dynamic of volatility skew, the Vanna-Volga adjustment is unnecessary.

It is worth noting that the Vanna-Volga adjustment does not apply to the European type model.

A double barrier option is described by two barriers: a lower barrier and a upper barrier. It is triggered if the underlying asset price hits the lower barrier or the upper barrier ( before expiration.

Typical double barrier option include:

A European double knockout option is a standard European option except that if the underlying aset price reaches outside of the two barriers during the option's lifetime, then the option is considered to be dead or pays a cash rebate at the breach time.

An American double knockout option is a standard American option except that if the underlying asset price is located outside of the two barriers during the contract's lifetime, then the option is considered to ceases to exist or pays a cash rebate at the breach time.

A double knockout option specification, for instance, includes an exercise time, a strike level, and a rebate value. In addition two barrier levels H_u and H_d, which depend continuously on time over the interval [0, T], must be specified. Note that the initial price of the underlying security S(0) must lie between the initial upper and lower barrier values, H_u(0) and H_d(0).

The double knockout option is knocked out the moment the underlying asset price reaches either the upper barrier or the lower barrier. If no barriers is triggered during the life time of the option, there is a payoff at expiry. Similiarly, a double knockin barrier option is converted to a vanilla option if either barrier is hit. Otherwise, it expires worthless.

The payoff from a long European double knockout call option is equal to that of a long, standard European call option, if the price of the underlying security does not cross either the upper or lower barrier during the time interval [0, T]; otherwise, as soon as one of these barriers is touched, a rebate value of R is received. Note that, of the double barrier options above, the double knockout option is the only option that allows for a rebate.

For knockout double barrier option, if we are long such a knockout annuity, we receive a fixed coupon annuity until the price of the underlying security crosses a preset barrier level; we then receive the accrued annuity since the last pay date. Note that only European exercise is permitted for the knockout annuities above, and no rebates are allowed.

A European double knockin becomes a standard European vanilla option if the underlying asset price hits either of the barriers during the option's lifetime. If the underlying price has always been inside the two barriers during the lifetime, it pays a cash rebate on the maturity date.

Similiarly, an American double knockin gives you a standard American option when the underlying price hits either of the barriers during the option’s lifetime. If the underlying price is always inside the two barriers during the option’s lifetime, it pays a cash rebate on the option maturity date.

A double binary one touch pays a cash rebate if the underlying asset price is located outside of the two barriers during the option's lifetime. The cash is paid either on the maturity date (European style) or at the time the barrier is reached.

A double digital no touch pays a fixed cash amount if the underlying asset price stays between the two barriers for the entire lifetime of the option.

A binary in pays a fixed cash amount if the underlying asset price is within the two barriers at the maturity, while a binary out pays a fixed cash amount if the underlying asset price is outside the two barriers at maturity.

For the spot history illustrateed above, if it is double no touch, then the condition is not satisfied; but if it is double one touch or one touch down no touch up, the condition is satified where point A is when the down barrier is touched.

A multi-window barrier option is a barrier option with a range of window periods. For each period, it is possible to define different levels of barriers and rebates. The product is also available for touch rebate options.

The option is a special case of a complex barrier option, where we can have multiple single and double partial barrier where a partial barrier is effective only on a subinterval of the full option term.

The term of the option is split into multiple windows. Each window has the characteristics of a double knock out partial barrier option with two partial knock out barriers, or a single knock out partial barrier option with one single partial knock oupt barrker.

The choice of In or Out must be consistent across windows. If any window style is In then for all windows style must be In, likewise for Out.

Basket barrier option is a barrier option on a basket of underliers. We observe each basket constituent stock price at each observation date. If on a observation time, all basket constituent stocks remain between their lower and upper barriers, then the barrier is not crossed.

There are several types of reference levels for computing payoff

For barrier hit probability calculations, We assume that stock prices are lognormal under a risk-neutral probability measure. In particular, we assume that the price of the stock in the basket satisfies

| Related Topics |