CPPI

FinPricing offers:

Four user interfaces:

- Data API.

- Excel Add-ins.

- Model Analytic API.

- GUI APP.

FinPricing provides valuation models for:

| 1. Constant Proportion Portfolio Insurance (CPPI) |

A constant proportion portfolio insurance (CPPI) is an exotic derivative that offers portfolio insurance in a dynamic asset allocation. The trading strategy allows investors to reallocate investment between a risky asset and risk-free asset. The risky asset could be equities, funds, commodities and risk-free asset could be treasury bond.

There is a floor portfolio value to guarantee a minimum payoff at maturity. CPPI trading strategy allocates more fund to the risky asset in upside markets but less in downside. It gives investors exposure to upside potential as well as downside protection. The capital potential and protection features are very appealing to market participants.

If the risky basket contains multiple risky assets, each asset may be equally weighted in most cases. As time passes, each asset may have different performance. The re-allocation strategy will allocate more weight to higher performance asset. In other words, the weights will be dynamically changed.

On a certain interval, e.g., daily or weekly, money is moved from risk-free basket to risky basket by selling bonds and buying equities, or vice versa.

| 2. CPPI valuation |

In a CPPI trading strategy, investment is rebalanced to a constant leverage in the risky asset. The leverage is funded by a market rate plus a spread. The daily accruals are complex. The compounding frequency is tied to the leverage rebalancing requency.

CPPI provides capital protection by face amount floor, make-whole floor, or anmuity floor. Porfolio valuation will be different under different floors.

Cushion is referred to as the distance between portfolio asset value and floor in percentage of notional. The allocation percentage to each basket depends on the cushion value. A cushion of full participation is given by:

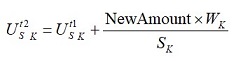

The weight for rebalancing is computed as

The new amount for balancing is allocated as:

If there is not enough fund to meet the rebalancing amount, all the available fund will be sold. The difference between the avaiable bund and the desired fund will be accumulated.

CPPI valuation includes many instances of theoretical rebalancing transactions which would theoretically give rise to cash but the cash that would be generated from such transactions should net to zero as the rebalancing is ideally meant to be cash-free.

For a risky asset with a management expense ratio (MER), the value should represent the price of a unit of the fund grossed-up by an amount that reflects the fees and expenses included in the management expense ratio applicable to units of the Fund, as specified by the CPPI contract. Adjustments are also made for fund distributions.

If a protection event has been triggered, the amount of bonds purchased is computed for the Floor, tender all asset units to finance the purchase. Adjustments on any excess or shortage on bonds purchased versus proceeds from asset units sold are made.

| 2. Related Topics |