FX Forward

FinPricing offers:

Four user interfaces:

- Data API.

- Excel Add-ins.

- Model Analytic API.

- GUI APP.

FinPricing provides valuation tools for the following FX products:

| 1. Currency Forward Introduction |

A currency forward or FX forward is a contract agreement between two parties to exchange a certain amount of a

currency for another currency at a fixed exchange rate on a fixed future date. Currency forwards are effective hedging

vehicles that allow buyers to indicate the exact amount to be exchanged and the date on which to settle in the forward

contract.

By locking into a forward contract to sell a currency, the seller sets a future exchange rate with no upfront cost.

Currency forward settlement can either be on a cash or a delivery basis, provided that the option is mutually

acceptable and has been specified beforehand in the contract. Forward contracts are one of the main methods used to

hedge against exchange rate volatility, as they avoid the impact of currency fluctuation over the period covered by

the contract.

Currency forwards are over-the-counter (OTC) instruments. Unlike standardized FX future,

a FX forward can be tailored to a particular amount and delivery period. If an investor will receive a cashflow

denominated in a foreign currency on some future date, that investor can lock in the current exchange rate by

entering into an offsetting currency forward position that expires on the date of the cashflow.

The currency forward contracts are usually used by exporters and importers to hedge their foreign currency payments

from exchange rate fluctuations. By using FX forward contracts, investors can protect costs on products and services

purchased abroad and protect profit margins on products and services sold abroad by locking-in exchange rates as much

as years in advance.

Currency forwards can also be used to speculate and, by incurring a risk, attempt to profit from rising or falling

exchange rates. A currency forward contract has credit risk. In the case that one of the parties is unable to fulfill

its obligation, the other party will have to sign another contract with a third party, thus being exposed to

market risk at that time. By locking-in the exchange rates at which the currency will

be bought, the party forfeits the opportunity of profiting from a favorable exchange rate movement.

| 2. Forex Market Convention |

One of the biggest sources of confusion for those new to the FX market is the market convention. We need to make clear the meaning of the following terms in the forex market first.

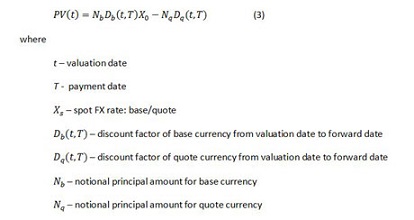

| 3. Pricing FX Forward Contracts |

The present value of a currency forward contract is given by

The above description tells us that FX forward rates and FX forward contracts are different subjects/entities. Sometimes people are confused about them.

| Related Topics |